Cyberattacks have become one of the most significant business risks facing organizations today. From ransomware attacks and data breaches to phishing campaigns and supply chain compromises, cyber incidents can disrupt operations, damage reputations, and result in substantial financial losses. As a result, many organizations invest heavily in information security programs to reduce their exposure to cyber threats.

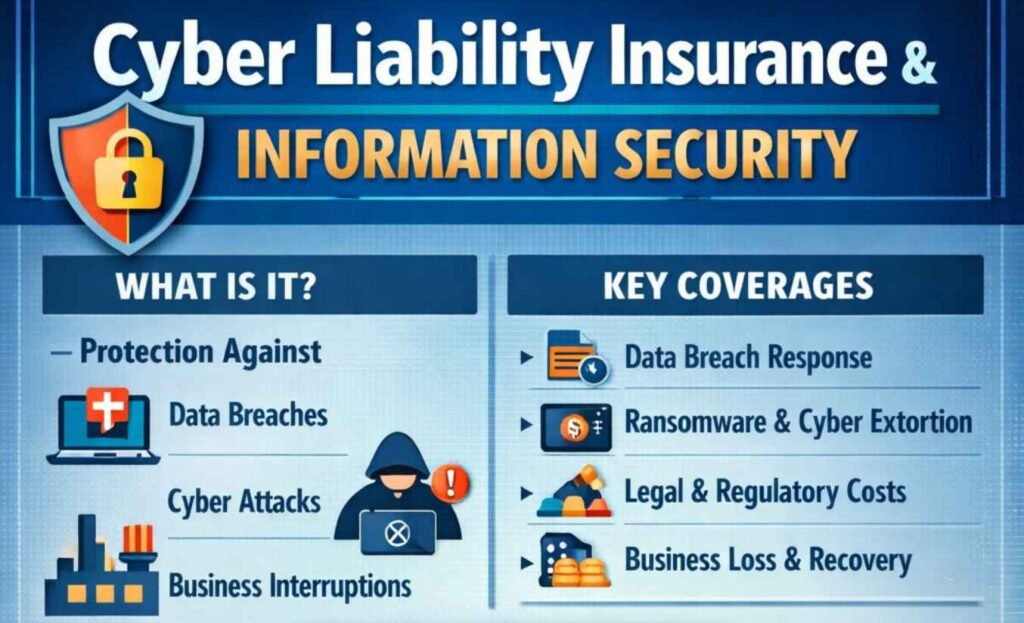

Cyber Liability Insurance covers financial losses from cyberattacks like data breaches, ransomware, and business interruptions, while Information Security refers to the practices and controls that prevent those risks. These concepts are complementary: strong information security measures often lower cyber insurance premiums and help with compliance, such as CMMC for defense contractors.

What is Cyber Liability Insurance?

Cyber Liability Insurance is a specialized business insurance policy that protects companies from financial losses caused by cyberattacks, data breaches, ransomware, or other cyber incidents. It covers costs like data recovery, legal fees, customer notifications, regulatory fines, and business interruption losses.

| Type | Examples | Details |

|---|---|---|

| First-Party | Forensic investigations, ransomware payments, system repairs, lost income | Handles recovery from incidents like hacking or extortion. |

| Third-Party | Lawsuits, settlements, fines for privacy violations | Covers claims from customers or regulators after a breach. |

CIA Triad Breakdown

| Principle | Definition | Examples |

|---|---|---|

| Confidentiality | Ensures data access only by authorized users. | Encryption, access controls, multi-factor authentication. |

| Integrity | Maintains data accuracy and prevents tampering. | Hashing, checksums, version control. |

| Availability | Guarantees timely access to data when needed. | Backups, redundancy, DDoS protection. |

Protect Your Business From Financial Hardship While Managing Information Security Risk

Cyber Liability Insurance safeguards businesses from financial losses due to cyber incidents like data breaches or ransomware, covering recovery costs while strong Information Security practices manage the underlying risks. Together, they minimize hardship by addressing both prevention and aftermath.

Strategies to Protect Finances

- Implement robust InfoSec: Use firewalls, employee training, multi-factor authentication, and regular audits to reduce breach likelihood and insurance premiums.

- Secure cyber insurance: Choose policies with first-party coverage (e.g., data recovery, business interruption) and third-party protection (e.g., lawsuits, fines).

- Pursue CMMC compliance: Tools like Armada’s CyberGap/CyberComply demonstrate diligence, aiding insurability for defense contractors.

Coverage Comparison

| Risk Area | InfoSec Role | Insurance Role |

|---|---|---|

| Data Breach | Prevention via encryption/access controls. | Notification, forensics, credit monitoring. |

| Ransomware | Detection/blocking malware. | Payments, recovery, lost income. |

| Business Downtime | Redundancy/backups. | Compensation for interruption losses. |

Build Your Customer Profile And Conquer The Cyber Liability Insurance Application

Cyber Liability Insurance applications require building a detailed customer (or business) profile to demonstrate low risk, helping underwriters approve coverage at competitive premiums. This involves self-assessing risks, documenting security measures, and submitting proof like policies and audits.

Steps to Build Your Profile

- Assess cyber risks: Identify sensitive data (e.g., customer info), system vulnerabilities, and potential impacts like revenue loss or fines.

- Gather business details: Compile company size, revenue, industry, past incidents, and current cybersecurity (e.g., firewalls, training).

- Document controls: Prepare IT policies, backup proofs, penetration test results, and certifications like CMMC.

- Complete questionnaire: Answer on operations, tech stack, access controls (MFA), EDR tools, patching, and incident history.

- Submit and review: Expect underwriter scrutiny; improve gaps (e.g., via Armada’s CyberGap) for approval.

What Is Information Security?

Information security refers to the processes, technologies, and policies used to protect information from unauthorized access, disclosure, modification, or destruction.

An effective information security program typically includes:

- Access controls

- Multi-factor authentication

- Security awareness training

- Endpoint protection

- Vulnerability management

- Data encryption

- Incident response planning

- Security monitoring

- Risk assessments

- Backup and recovery procedures

The primary objective of information security is to reduce the likelihood and impact of cyber incidents.

Organizations often invest in security technologies and compliance frameworks such as:

- NIST Cybersecurity Framework

- NIST SP 800-171

- CMMC

- ISO 27001

- SOC 2

- HIPAA Security Rule

These frameworks help establish structured approaches to managing information security risks.

Why Information Security Alone Is Not Enough

A common misconception is that organizations with strong security controls do not need cyber liability insurance.

In reality, no security program can eliminate all risk.

Consider a company that has implemented:

- Multi-factor authentication

- Endpoint detection and response

- Security awareness training

- Continuous monitoring

- Regular vulnerability assessments

Despite these protections, an employee may still fall victim to a sophisticated phishing attack. An attacker may exploit a previously unknown software vulnerability. A trusted vendor may experience a breach that affects multiple customers.

Even organizations with mature cybersecurity programs can suffer significant losses from incidents that bypass existing defenses.

Information security reduces risk, but it does not eliminate financial exposure.

Cyber liability insurance exists to help organizations manage the residual risk that remains after security controls are implemented.

The Relationship Between Cyber Insurance and Security

Cyber liability insurance and information security are often viewed as separate disciplines, but they are closely connected.

Insurance providers increasingly evaluate an organization’s security posture before issuing or renewing cyber insurance policies.

Many insurers now require organizations to demonstrate the implementation of security controls such as:

- Multi-factor authentication

- Endpoint protection

- Email security

- Data backup procedures

- Incident response plans

- Employee security awareness training

Organizations with stronger security programs may qualify for:

- Lower premiums

- Higher coverage limits

- Better policy terms

Conversely, companies with weak security practices may face higher premiums or difficulty obtaining coverage.

This relationship has created a situation where improving information security can directly influence cyber insurance outcomes.

A Practical Example

Imagine two manufacturing companies with similar revenue and business operations.

Company A

The organization has:

- Multi-factor authentication

- Security awareness training

- Endpoint detection tools

- Regular vulnerability scanning

- Incident response planning

Company B

The organization has:

- Basic antivirus software

- Weak password policies

- No formal security training

- No incident response procedures

When applying for cyber liability insurance, Company A is likely to be viewed as a lower-risk applicant because it has implemented recognized security controls.

Company B may face higher premiums, reduced coverage options, or additional underwriting requirements.

This example illustrates how insurers increasingly consider information security maturity when assessing cyber risk.

Common Cyber Insurance Coverage Areas

Cyber liability policies vary significantly, but coverage generally falls into two categories: first-party coverage and third-party coverage.

First-Party Coverage

First-party coverage helps organizations recover from direct losses resulting from cyber incidents.

Examples include:

- Business interruption losses

- Data recovery costs

- Incident response services

- Forensic investigations

- Crisis management expenses

Third-Party Coverage

Third-party coverage addresses claims brought by customers, partners, or other external parties.

Examples include:

- Legal defense costs

- Privacy lawsuits

- Regulatory investigations

- Settlement expenses

Organizations should carefully review policy language to understand what is and is not covered.

Why Incident Response Matters

One often overlooked benefit of cyber liability insurance is access to incident response resources.

Many insurers maintain networks of approved:

- Digital forensic firms

- Breach attorneys

- Crisis communications specialists

- Recovery consultants

During a major cyber incident, organizations may gain immediate access to experienced professionals who can assist with investigation and recovery efforts.

For small and mid-sized businesses without dedicated incident response teams, this support can be extremely valuable.

Compliance and Insurance Considerations

Organizations pursuing compliance certifications such as CMMC, NIST SP 800-171, ISO 27001, or SOC 2 often assume that compliance automatically guarantees insurance coverage.

This is not always the case.

Compliance frameworks improve security maturity, but insurance providers may evaluate additional factors, including:

- Claims history

- Industry sector

- Revenue size

- Third-party dependencies

- Ransomware exposure

- Security governance practices

Businesses should avoid assuming that compliance certification alone satisfies all insurance requirements.

Instead, cyber insurance and compliance should be viewed as complementary components of a broader cyber risk management strategy.

Common Mistakes Organizations Make

Several mistakes frequently occur when organizations approach cyber insurance and information security.

Treating Insurance as a Substitute for Security

Cyber insurance is not a replacement for security controls.

Insurance may help recover financial losses, but it cannot restore customer trust or prevent operational disruption.

Failing to Understand Policy Exclusions

Many organizations purchase policies without fully reviewing exclusions and coverage limitations.

Understanding policy details is critical before an incident occurs.

Ignoring Vendor Risk

Third-party vendors can create significant exposure.

Organizations should evaluate both their own security posture and the security practices of key partners.

Neglecting Incident Response Planning

Insurance coverage is more effective when organizations have documented response procedures and trained personnel.

Building a Balanced Cyber Risk Strategy

The most effective organizations recognize that cyber resilience requires multiple layers of protection.

A balanced strategy often includes:

- Strong information security controls.

- Security awareness training.

- Regular risk assessments.

- Vendor risk management.

- Business continuity planning.

- Incident response preparation.

- Cyber liability insurance.

Each component addresses a different aspect of cyber risk.

Security controls help prevent incidents.

Risk management helps prioritize resources.

Insurance helps manage financial consequences.

Together, they create a more resilient organization.

Why It Matters

A strong customer profile in a Cyber Liability Insurance application like at Cyber-Armada matters because it allows underwriters to precisely evaluate your business’s cyber risks, security posture, and potential financial exposure, leading to faster approvals and lower premiums. Detailed documentation of controls like MFA, patching, backups, and CMMC compliance demonstrates proactive risk management, reducing perceived vulnerabilities and avoiding rejections or exclusions.

During claims, the profile verifies that you maintained promised practices, preventing denials and ensuring coverage for costs like breach forensics or lost revenue, which average millions per incident. For defense contractors using tools from Armada Cyber Defense, a robust profile not only secures insurability but also aligns with compliance needs, saving up to 50% on premiums while protecting against catastrophic financial hardship.

Wrap-up

Cyber liability insurance and information security serve different but equally important purposes. Information security focuses on reducing the likelihood and impact of cyber incidents through technology, processes, and governance. Cyber liability insurance helps organizations manage the financial consequences when those incidents occur despite existing safeguards.

Neither approach is sufficient on its own. Strong security controls without insurance may leave an organization exposed to significant financial losses. Insurance without adequate security controls may result in higher premiums, limited coverage, or increased operational risk.

As cyber threats continue to evolve, businesses must recognize that cyber resilience requires both prevention and recovery capabilities. By combining effective information security practices with appropriate cyber liability insurance coverage, organizations can better protect their operations, reputation, customers, and long-term business objectives.

FAQ’s

What Does Cyber Liability Insurance Cover?

It reimburses first-party costs like breach response, lost revenue, and ransomware payments, plus third-party claims for data exposure or service disruptions.

Does It Cover Ransomware in OT Systems?

Yes, it covers Ransomware in OT Systems

What Security Requirements Do Insurers Impose?

Mandatory MFA, vulnerability scans, backups, and OT segmentation; non-compliance raises premiums 25-45% or voids coverage.

How Much Does It Cost?

Small manufacturers pay USD 2K to USD 10K yearly for $1M coverage, scaling with revenue and risks; ransomware trends keep rates firm but accessible.