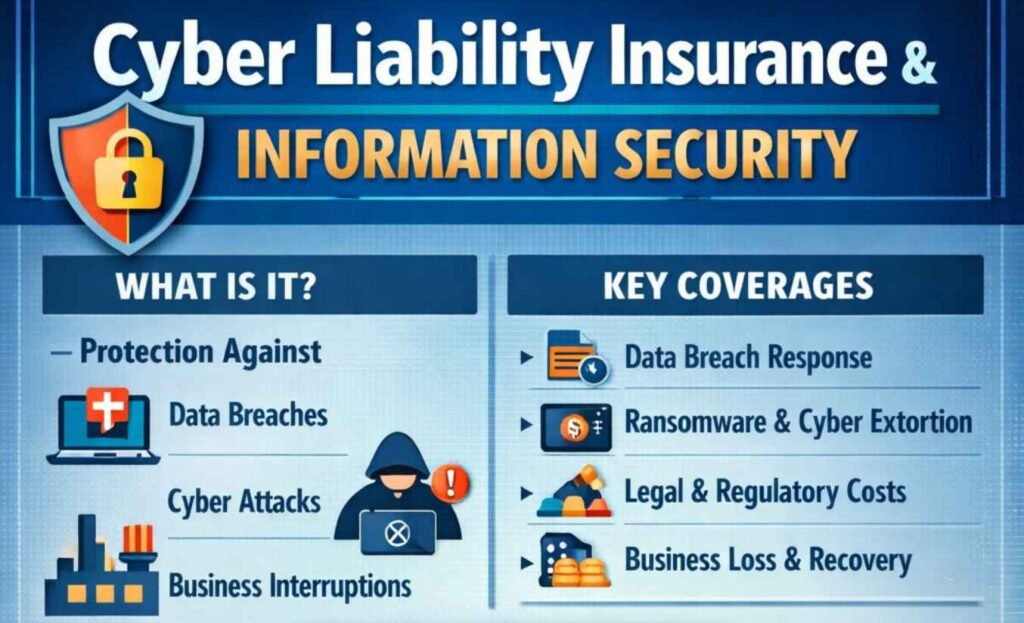

Cyber Liability Insurance covers financial losses from cyberattacks like data breaches, ransomware, and business interruptions, while Information Security refers to the practices and controls that prevent those risks. These concepts are complementary: strong information security measures often lower cyber insurance premiums and help with compliance, such as CMMC for defense contractors.

What is Cyber Liability Insurance?

Cyber Liability Insurance is a specialized business insurance policy that protects companies from financial losses caused by cyberattacks, data breaches, ransomware, or other cyber incidents. It covers costs like data recovery, legal fees, customer notifications, regulatory fines, and business interruption losses.

Coverage Types

Policies typically split into first-party (your direct costs) and third-party (liabilities to others) protections.

| Type | Examples | Details |

|---|---|---|

| First-Party | Forensic investigations, ransomware payments, system repairs, lost income | Handles recovery from incidents like hacking or extortion. |

| Third-Party | Lawsuits, settlements, fines for privacy violations | Covers claims from customers or regulators after a breach. |

Information Security (InfoSec) is the practice of protecting data and information systems from unauthorized access, misuse, disclosure, disruption, or destruction. It focuses on ensuring the confidentiality, integrity, and availability of information, often referred to as the CIA triad.

This means that only authorized individuals can access data, the information remains accurate and unaltered, and it is available when needed. Information security involves a combination of technologies, processes, and policies such as encryption, firewalls, access controls, and regular monitoring to defend against cyber threats like hacking, malware, ransomware, and data breaches.

In today’s digital world, it plays a critical role in safeguarding sensitive personal, financial, and business information, helping organizations maintain trust, comply with regulations, and ensure smooth business operations.

CIA Triad Breakdown

| Principle | Definition | Examples |

|---|---|---|

| Confidentiality | Ensures data access only by authorized users. | Encryption, access controls, multi-factor authentication. |

| Integrity | Maintains data accuracy and prevents tampering. | Hashing, checksums, version control. |

| Availability | Guarantees timely access to data when needed. | Backups, redundancy, DDoS protection. |

Protect Your Business From Financial Hardship While Managing Information Security Risk

Cyber Liability Insurance safeguards businesses from financial losses due to cyber incidents like data breaches or ransomware, covering recovery costs while strong Information Security practices manage the underlying risks. Together, they minimize hardship by addressing both prevention and aftermath.

Strategies to Protect Finances

- Implement robust InfoSec: Use firewalls, employee training, multi-factor authentication, and regular audits to reduce breach likelihood and insurance premiums.

- Secure cyber insurance: Choose policies with first-party coverage (e.g., data recovery, business interruption) and third-party protection (e.g., lawsuits, fines).

- Pursue CMMC compliance: Tools like Armada’s CyberGap/CyberComply demonstrate diligence, aiding insurability for defense contractors.

Coverage Comparison

| Risk Area | InfoSec Role | Insurance Role |

|---|---|---|

| Data Breach | Prevention via encryption/access controls. | Notification, forensics, credit monitoring. |

| Ransomware | Detection/blocking malware. | Payments, recovery, lost income. |

| Business Downtime | Redundancy/backups. | Compensation for interruption losses. |

Build Your Customer Profile And Conquer The Cyber Liability Insurance Application

Cyber Liability Insurance applications require building a detailed customer (or business) profile to demonstrate low risk, helping underwriters approve coverage at competitive premiums. This involves self-assessing risks, documenting security measures, and submitting proof like policies and audits.

Steps to Build Your Profile

- Assess cyber risks: Identify sensitive data (e.g., customer info), system vulnerabilities, and potential impacts like revenue loss or fines.

- Gather business details: Compile company size, revenue, industry, past incidents, and current cybersecurity (e.g., firewalls, training).

- Document controls: Prepare IT policies, backup proofs, penetration test results, and certifications like CMMC.

- Complete questionnaire: Answer on operations, tech stack, access controls (MFA), EDR tools, patching, and incident history.

- Submit and review: Expect underwriter scrutiny; improve gaps (e.g., via Armada’s CyberGap) for approval.

Why It Matters

A strong customer profile in a Cyber Liability Insurance application like at Cyber-Armada matters because it allows underwriters to precisely evaluate your business’s cyber risks, security posture, and potential financial exposure, leading to faster approvals and lower premiums. Detailed documentation of controls like MFA, patching, backups, and CMMC compliance demonstrates proactive risk management, reducing perceived vulnerabilities and avoiding rejections or exclusions.

During claims, the profile verifies that you maintained promised practices, preventing denials and ensuring coverage for costs like breach forensics or lost revenue, which average millions per incident. For defense contractors using tools from Armada Cyber Defense, a robust profile not only secures insurability but also aligns with compliance needs, saving up to 50% on premiums while protecting against catastrophic financial hardship.

FAQ’s

What Does Cyber Liability Insurance Cover?

It reimburses first-party costs like breach response, lost revenue, and ransomware payments, plus third-party claims for data exposure or service disruptions.

Does It Cover Ransomware in OT Systems?

Yes, it covers Ransomware in OT Systems

What Security Requirements Do Insurers Impose?

Mandatory MFA, vulnerability scans, backups, and OT segmentation; non-compliance raises premiums 25-45% or voids coverage.

How Much Does It Cost?

Small manufacturers pay USD 2K to USD 10K yearly for $1M coverage, scaling with revenue and risks; ransomware trends keep rates firm but accessible.